Is the Chase Sapphire Preferred Credit Card Worth the $95 Annual Fee?

Thank you Amanda for asking me why the Chase Sapphire Preferred credit card was not used on my recent trip to Cabo. Great question Amanda, let me explain why…

There is no doubt that the Chase Sapphire Preferred is a great credit card. Double points on travel and dining purchases is awesome. Transferable points to many of the best airline and hotel loyalty programs is awesome. No foreign transactions fees and no annual fee (for the first year) is awesome. I think that if you could only have 1 Chase credit card, most people would say the Chase Sapphire Preferred is the best card (we will assume you are not a business owner). I totally agree 100%. But what about the second year and the third year and the fourth year when you have to pay the $95 annual fee. Is it still worth it?

Yes and no.

It really depends on your situation and whether or not you have a Chase Ink Bold/Plus Business credit card. In my situation, I do have 2 Chase Ink Bold Business credit cards, so the “transferable points to many of the best airline and hotel loyalty programs is awesome” statement is no longer as important. This is because the Chase Ink Bold and the Chase Sapphire Preferred have the same transfer abilities.

Let’s take a look at the other statement, “double points on travel and dining purchases is awesome.” I’m not sure about you, but I have several other travel reward credit cards from Chase. I have the following credit cards open:

- Chase Freedom

- I only use this credit card for transactions that fall into the 5x/5% cash back categories.

- Sometimes that means restaurants (like last quarter), so the 5x/5% cash back was actually better than the Chase Sapphire Preferred.

- Chase Marriott Rewards Premier

- 5x at Marriott vs. 2x with the Chase Sapphire Preferred (let’s not argue about the value of Marriott points).

- 2x on rental cars, airfare, and restaurants = 2x with Chase Sapphire Preferred

- 1 free night at a category 1-5 Marriott hotel for paying the $85 annual fee (I got a retention offer for another free night certificate this year – link)

- Chase Hyatt

- 3x at Hyatt vs. 2x with the Chase Sapphire Preferred (let’s not argue about the value of Hyatt points).

- 2x on rental cars, airfare, and restaurants = 2x with Chase Sapphire Preferred

- 1 free night at a category 1-4 Hyatt hotel for paying the $75 annual fee

- Chase IHG Rewards Club

- 5x at IHG vs. 2x with the Chase Sapphire Preferred (let’s not argue about the value of IHG points).

- 2x on gas stations and grocery stores

- 2x on restaurants = 2x with Chase Sapphire Preferred

- 1 free night at any IHG hotel for paying the $49 annual fee

- Chase Southwest Airlines Premier

- 2x on Southwest Airlines flights = 2x with Chase Sapphire Preferred

- 2x on hotels and rental cars = 2x with Chase Sapphire Preferred

- 6,000 Southwest Airlines miles (worth ~$85) for paying the $95 annual fee (I got a 3,000 mile retention offer this year – link)

- Chase Southwest Airlines Plus

- 2x on Southwest Airlines flights = 2x with Chase Sapphire Preferred

- 2x on hotels and rental cars = 2x with Chase Sapphire Preferred

- 3,000 Southwest Airlines miles (worth ~$43) for paying the $65 annual fee (I plan on asking for a retention offer when the annual fee comes due, or closing the credit card)

- Chase Ink Bold (a Visa and a MasterCard)

- 5x at office supply stores, cell phone/cable/internet bills > 1x with Chase Sapphire Preferred

- 2x at hotels = 2x with Chase Sapphire Preferred

- 2x at gas stations > 1x with Chase Sapphire Preferred

- $95 annual fee (I got a $95 statement credit retention offer this year – link)

Let’s take a look at the last statement above, “no foreign transactions fees and no annual fee (for the first year) is awesome.” All of the credit cards above, with the exception of the Chase Freedom and the Chase Southwest Airlines Plus credit card have no foreign transaction fees, so I always leave those at home when travelling abroad. Some of the Chase credit cards above have annual fees, some of the annual fees are waived the first year, and some annual fees are not. All the cards that have annual fees offer something worth more than the annual fee, otherwise I call looking for a retention bonus or I will close/downgrade/convert the card into a different card.

Side note: I’m not sure 5x at gas stations and Kohl’s is worth using my Chase Freedom internationally when I have to pay “3% of each transaction in U.S. dollars.” Also, when I was in Cabo 2 weeks ago, I saw 2 Office Max stores and a Staples and I was tempted to go inside and see what the gift card situation was like, but I unfortunately did not make it to a store.

When I am home, I always use my Citi Forward credit card since it pays 5% cash back at all restaurants. I know this card is no longer accepting new applications, but 5% cash back is much better than 2x with the Chase Sapphire Preferred. When I travel international, I have a choice of which Chase credit card to use when paying for restaurants. The Chase Hyatt, Marriott, and IHG credit cards all offer 2x on restaurants. Since I personally get the most value out of Hyatt points, I always use my Hyatt credit card for international restaurant purchases.

As for travel, I will break travel into rental cars, hotels, and airfare. For rental cars, most of the personal cards offer 2x on rental car purchases, so I tend to use my Chase Hyatt for rental cars. As for hotels, I have all the major hotel credit cards (Hyatt, Marriott, IHG, Hilton, SPG, and Club Carlson). If I am not staying at one of those chains, I use my Chase Ink Bold to earn 2x on the purchase. As for airfare, I have both Chase Southwest Airlines credit cards, I used to have United and British Airways credit cards, but those cards weren’t worth the annual fee, so I closed those cards. I have a few American Airlines credit cards, a few Alaska Airlines credit cards, and my American Express Premier Rewards Gold which earns 3x Membership Reward Points on airline purchases. If it is an international airline purchase, I use my Chase Hyatt to earn 2x with no foreign transaction fees vs. using the PRG that charges 2.7% foreign transaction fees.

So that’s it.

That is my long winded attempt to explain why I no longer have a Chase Sapphire Preferred credit card. I originally downgraded the card to the no annual fee Chase Sapphire, but that card was worthless, so I converted that card to the no annual fee Chase Freedom for the 5x/5% cash back categories. In essence, I believe the more Chase credit cards you have (and an Ink Bold/Plus business credit card), the less value you get out of your Chase Sapphire Preferred.

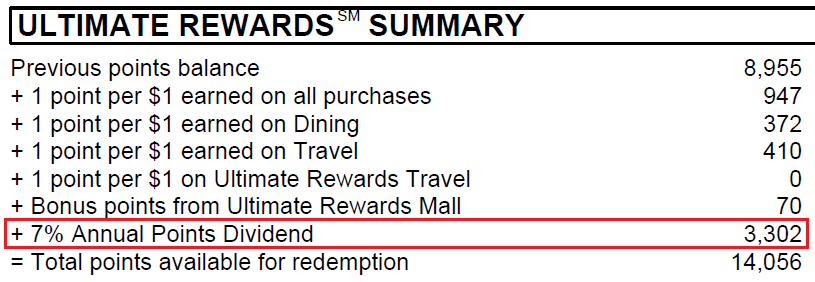

Now that the 7% annual bonus is gone, I see even less of a reason to keep the card and pay the annual fee. I only received 3,302 Chase Ultimate Reward Points for my 7% dividend.

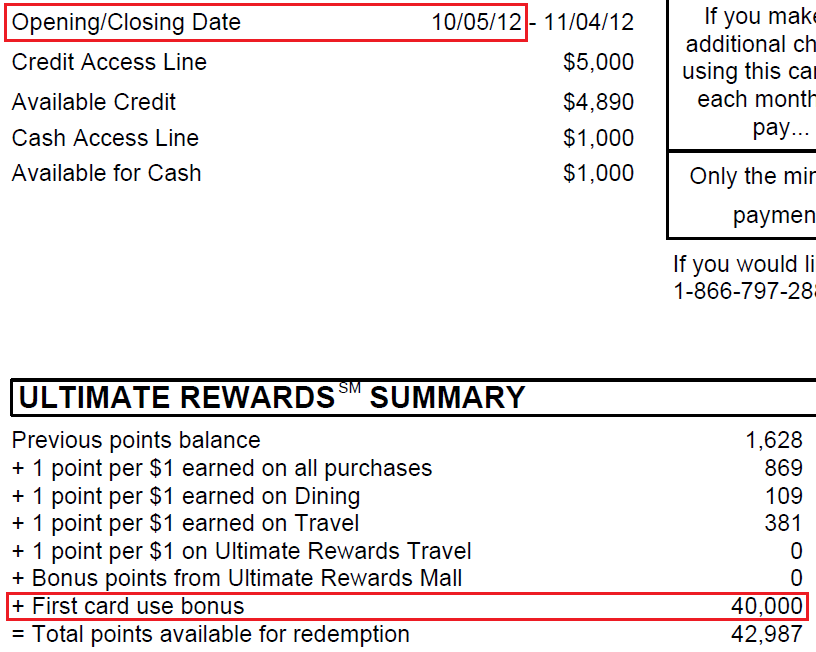

But the best part of closing the Chase Sapphire Preferred… the ability to reapply and get the sign up bonus again! I just have to wait 2 years after October 5, 2012. I will go for the Chase Sapphire Preferred during my December/January App-O-Rama. If you can remember back to 2012, the Chase Sapphire Preferred was offering 40,000 Chase Ultimate Reward Points… after your first purchase! Those were the good ol’ days…

So now that you read my whole story (or just scrolled down to the bottom of this post to look at the poll), let me know what you think:

If you have any questions, please leave a comment below.

P.S. If you do not have a Chase Sapphire Preferred, please consider using my Chase Sapphire Preferred referral sign up link on my credit card page. Thank you!

I have mixed up my card usage as needed, but I have seen posts where people will tell you not to mix personal and business charges on the Chase Ink cards. How do you deal with that?

I have never had a problem using my Chase Ink Bold for “non business” spend. If Chase ever asked me, I’m sure I could tell them the purchase is related to my business. Honestly, I think as long as you pay your credit card bill on time, Chase doesn’t care what you buy with their credit cards. As far as I know, business credit cards have less consumer protections (warranty, travel protection, etc.) than personal credit cards, so they don’t want consumers to be hurt by using a credit card that does not protect them.

Transfer your Sapphire credit line to the Freedom, which has no annual fee, then cancel and get bonus again. Also, did you know you can transfer Chase Freedom points to your Ink for use in Ultimate Rewards? You can only transfer Freedom points to earn UR’s if you have Ink card(s), or Sapphire (but they are UR transferrable).

Yes, that is a good point. I should have mentioned that in the post. Good catch!

Very helpful post, thank you!

Thanks Adam, glad you liked it! Any other credit cards you want me to “review”?

Chase may be seeing people switch spend from Sapphire Preferred…I recently switched spend to a Barclay’s Arrival+ and within weeks Chase bumped the credit access line on my Sapphire Preferred…a hint perhaps?

Wow, did you make a big switch in spending (like $5000 per month from the CSP to the Barclays Arrival+?

Adam, I do a lot of cruising and get 2X with the CSP. What would be a good replacement? I have the CIB and IHG cards. Good post!

The Barclays Arrival+ is a good replacement I think. It might be worth looking at a cruise line related credit card if you are loyal to one cruise line, but I think the rewards on those cards are pretty bad.

Very informative post! In applying for the Sapphire again, do you wait 2 years from when you closed the account? I thought you can’t receive the bonus again once you’ve had it in the past.

Chase recently changed the TOC for some of their credit cards whereby you can get the sign up bonus again. I believe you have to wait at least 2 years from the date the bonus was paid out. So if I got the CSP Jan 1, 2012, but I didn’t get the sign up bonus until March 30, 2012, I would have to wait until at least March 30, 2014 to get the sign up bonus again. I would play it safe and wait 2 years plus a few months so that you don’t jump the gun and apply too early.

Couple things:

The credit card companies only care if you use your business card for non-business usage if you spectacularly abuse it (such as only charge disney tickets and ice cream parlors), never charges that pass the business sniff test, since their credit business is regulated differently for business and personal. They only care if they are audited by the government and are deemed to being offering business lines for personal use. I talked with a Chase VP a few years ago about this and he said they are really, really lax on this. Just throw in a Staples or Costco or Sam’s purchase every now and then and you’ll be fine.

Also, I agree with abandoning the Sapphire nearly 100% of the time if you already have an Ink. The $95 just isn’t worth it. With another BIG reason being that Chase will eventually deny you more credit either due to the number of cards you have or the total line or both. I got denied on my 5th Chase card simply because I had too many accounts open. Didn’t matter that the credit lines weren’t huge. Two friends also told me they were stopped cold based on numbers of Chase cards and both missed the 100K Avios promos. The Sapphire isn’t worth that risk if you own an Ink.

Side note: You have a lot of Chase cards! Congratulations. It’s a great company to work with.

I would say 90% of the charges on my Ink card are from Staples, 5% for AT&T and cable TV/internet and then 5% for other. I have 6 personal cards with Chase, all have $5,000 credit line. Most recon calls say you need to have at least $5,000 on the credit line to be approved for the card, but you can always borrow credit from existing credit cards to make the credit line lower. For me, my 2 Chase SWA credit cards are the first on the chopping block. I got them for the sign up bonus and pay the annual fee and break even with the bonus points they offer. What Chase rep could argue with this statement “I don’t need 2 Chase SWA credit cards, so I will close 1 of them.”

awesome post grant. love the “non-pump” nature of the post and the very straightforward breakdown. very enjoyable read.

in the end, i guess it depends on what other cards you have. if you dont have ANY other credit cards and youre spending $9500 or more on travel and dining, then this would be worth it even at a strict cash-back cost. of course, retention calls, etc. can be thrown in the mix to help too …..

i kinda want it too but really only because its heavy and metallic lol. otherwise i have too many other cards already as it is ….

Chase is slowly rolling out more credit cards that are metallic and have Chip and Sig. The Marriott card is like that, but I’m sure more will be like that in the near future.

I agree that it really depends on your situation. It seems like all of the “anti-bloggers” are crapping all over the CSP, and I can understand why, but for some people (like myself), it’s an amazing card.

I have a Freedom (which I love), but I don’t have an Ink. I don’t own a business and honestly, I’m not willing to pretend to have one.

45% of my spending is on restaurants and travel (almost all for work). I also spend enough for work each month to meet my travel needs without needing to apply for more cards.

Everyone has a different situation, you just have to find the perfect situation that fits your lifestyle/shopping habits. If you earn enough points with the CSP, stick with that. Out if curiosity, how much do you typically charge on your CSP per month?

GAM: You may not be willing to pretend you have one, but Chase wants you to pretend you have one :)……………………as long as you use it.

10-15k per month. Maybe 1-2k in MS…everything else is legitimate spending.

Nice, you should have plenty of UR points. If you need helping spending them, you know who to ask ;)

I agree. The more chase cards u have, the less you need the CSP after the first year. I downgraded from CSP to the regular sapphire to avoid the annual fee. later I will apply for another chase card and close sapphire to use the credit limit for new card. Having just gotten my arrival + and my Cap 1 Venture card also makes CSP less valuable to me. On a side note I recently found out arrival plus card will give you points for writing short travel stories and sharing pics on their Barclay card travel review web site. I haven’t seen much written on this feature so maybe you could write a post on this Grant.

3 other things about Barclay’s Arrival card:

– You can’t redeem any expense that’s less than $25, even by aggregating small expenses (found that out the hard way with a bunch of small taxi receipts)

– The bank rotates the same offer through its credit card portfolio at least once a year: Spend $750 in 3 consecutive months and get 5000 Arrival points (which is really like 5500 once redeemed). They just finished this offer on the Arrival and are now doing it on the uPromise

– 3 months ago they offered 4 extra points on top of the standard 2 for buying Amex gift cards. So, you’d get 6.6% back if redeemed for travel. Barclays has a date by which all vendors must pay their bonuses out even if they’re not paid by the merchant. In this case, they gave me $600 even though Amex hadn’t paid them.

I don’t have a Barclays card, so I’m not sure I can write a review. Someone feel free to use my posts and pics to get free Barclays points.

On it. Thanks Grant. Best travel blogger ever. Best readers too, I don’t think I have ever seena negative remark. Not sure if Grant edits those out but still its a nice change compared to what I’m used to from other sites

Grant is the bestest blogger in the world!

(Ok that last part was edited by me)

I get maybe 1 or 2 negative comments a month. Sometimes people comment on old posts or pages that I wrote a while ago that are out of date.

Thanks Grant for the wonderful post and I am happy that many enjoy this topic! by the way, for Chase Marriott and Hyatt cards, I won’t get UR points but it will be in Marriott or Hyatt points, correct?

Also, does Chase recon call center open on Monday Labor day weekend? it’s Sept 2, the last day to apply for limited time increased sign up bonus for Chase United and I plan to apply on that day.

Yes, if you use a Chase Marriott or Chase Hyatt credit card, you will earn either Marriott points or Hyatt points for your purchases. I am not sure if/when Chase’s reconsideration department is open/closed. I would try calling early Monday morning. If they are closed, you can call back early Tuesday morning (September 2). If you apply for the Chase United Airlines credit card, you should be able to reach the recon department, if needed, in time.

Thanks, do you think it’s ok if I apply on Monday (labor day) and if not approved I will call on Tue if the recon not open on labor day.

Yes, that is a good idea. If you have time, you may want to apply Thursday or Friday morning, but I’m sure you will have no problem getting instantly approved or approved after a quick call to the recon department.

Thanks Grant! you’re the best!

Thanks Amanda, I try!

Grant, I think I cannot apply today or Friday, as I just got my Chase CSP on end of June and it’s not 90 days yet so I am trying to apply on the last day of the promotion to increase my chance of getting approved.

I am confused now and need your help. The Marriott (70k bonus, until Sept 15) or United card (50k bonus, until Sept 2)? I only can apply for one card and both of these cards have limited sign up bonus that will end in September so it made me confused.

I think the Marriott 70k offer has been around quite a while (I applied from FlyerTalk 1.5 years ago). Go for the United offer since that sign up bonus hasn’t been around in a while.

Thanks Grant~

Please pardon me if this has been discussed before in your blog or you already wrote about this, but I am just wondering if you already have or will write a guide about searching award availability in oneworld airlines by using AAdvantage miles, as well as when the award seat availability open up on Cathay/JAL (I guess these 2 are the most important as they are the top 2 best airlines that have better premium class seat and service for long haul flights compared to others) how to upgrade/change the award via phone, the fee, etc.

For example, scenario 1: booked an award seat in economy class in AA metal using AA miles to secure the award flight, then decided to change and upgrade it to Cathay/JAL flight in business class. (same destination).

Scenario 2: booked an award seat in first class in AA metal using AA miles to secure the award flight, then decided to change to JAL/Cathay flight in first class (same destination – no change in class, only the flight, date and time).

Also, I have question, if I have some miles in Alaska Airlines account and some in AA, how to combine both miles to book Cathay’s business or first class? If using Alaska Airline miles alone is not enough, have to combine both Alaska and American so the total mileage would be enough to book for Cathay’s business class.

I think it would be beneficial and helpful for a lot of people who are not familiar with this. If you already wrote about this, please kindly share the link to that post. Thanks a lot again!

I have these 2 guides for making AA bookings with miles: http://travelwithgrant.com/trip-reports/lax-dus-bcn-with-aa-miles-and-mad-muc-lax-with-ua-miles/

http://travelwithgrant.com/trip-reports/sna-dfw-mad-agp-with-aa-miles-on-aa-and-iberia/

I think both if your scenarios would involve an award cancellation/redeposit of AA miles fee of $150 per person. You would have to cancel the existing reservation, pay the $150 fee and then book the new reservation. You should be able to do it all over the phone with the same rep(s). You won’t be able to change for free unless there was a schedule change or aircraft swap. You might be waiting a whole for that and miss the opportunity to change to the route you want.

Thanks for the guide and trip report, I already bookmarked it and it will be my reading material tonight!

By the way, I was browsing around to find any related Cathay and AA related booking/upgrades and stumbled upon this post by another blogger and I read that he was able to upgrade his seat from business to first on Cathay using AA miles without any fee (he just paid the difference of mileage needed) and he mentioned that as long as the origin and destination are the same, there is no fee? Can you please clarify about this?

http://www.noobtraveler.com/how-to-upgrade-a-cathay-pacific-award-ticket-booked-with-aa-miles/

I have no experience upgrading from international business to first. Try leaving a comment on that post or emailing him. Hopefully he can provide helpful information.

Excellent analysis of the CSP. In my case, I have a huge credit line on it, and I just got an Ink Bold (already have the Ink Plus) and they gave me crappy $5K credit lines. I believe I can’t transfer any portion of that personal credit line with my CSP to either of the Inks, so I’m going to keep the CSP open, just for credit line. And then work on getting my business credit lines increased. It’s worth it for me to pay the $95 CSP annual fee. I think if I downgraded to a regular Chase Sapphire w/o an annual fee, I would maybe lose that large credit line… or am I incorrect?

If you downgrade/convert a Chase Sapphire Preferred to the basic Chase Sapphire or the Chase Freedom, your credit line will remain the same. As far as I know, the Chase Ink Bold doesn’t have a credit limit. It is a charge card with no preset spending limit.

Oh, I didn’t know that. Thanks for the tip. My CSP renewal is coming up soon, and if I can keep the credit line, then I’ll downgrade. No reason to keep paying the fee if I can preserve the credit line. As for the Chase Ink Bold. I know it’s a charge card, but they still said something about the $5K, although they tried to explain it’s not a limit, but it sounded like one. They said something about analyzing spending patterns to increase that, so we’ll see how it goes… Thanks again!

I forget the exact wording, but it’s like a flexible credit limit, you can spend more than $5,000 per month and they will adjust the flexible limit based on your spending patterns.

Wow Grant. When you explain the numerous amount of credit cards that you have under your belt it definitely makes sense that the CSP becomes worthless. I just think its crazy to have that many credit cards especially when most of them have an annual fee and I don’t see how you can maximize every CC to justify the annual fee.

I try to stick to 3 CCs so that I can maximize the rewards as well as reduce the annual fees (Yes I know I can call and ask for retention offers which may or may not work). I do agree with your statement that if you have the Chase Ink cards its a bit redundant to have the CSP in terms of 1:1 network access to partner airlines.

I am sure I have more Chase cards than the average person. From Chase, the best cards are hotel cards and cards with no annual fees. It is hard to justify the annual fee on the airline credit cards unless you typically check bags. Luckily the Southwest cards offer bonus points to partially offset the annual fee, but I get the least value from those cards. I book 100% of SWA flights with SWA points and only charge the $5.60 taxes/fees to the SWA credit card.

Pingback: Random News: CSP Poll Results, Back 2 School Blogger Report Card, Staples Free After Rebate Paper, Korean Kit Kat Bar, and New AMEX Offers for AMEX Hotels, Paperless Post, and Cole Haan | Travel with Grant

Is it possible to downgrade the Chase Southwest Card to a Freedom Card even if you already have another Chase Freedom Card?

I’m not sure if you can convert from a SWA credit card to a Freedom credit card. You can ask them but it might not be possible.

I have a CSP, where my wife is added as an authorized user. I’m thinking of downgrading the CSP to a Chase Freedom card during Feb’2015, when I’m due for the next annual fee. Can my wife apply for a new CSP card while she is currently an authorized user on my card? If yes, is it better for her to apply for a new CSP after I downgrade to Chase Freedom or before that?

If you have a Chase Sapphire Preferred and your wife is the authorized user, and she will also have a Chase Sapphire Preferred. If you downgrade your card to the Chase Freedom, she will get a new Chase Freedom. She will still be eligible for the sign up bonus on the Chase Sapphire Preferred, it doesn’t really matter if she gets it before or after you downgrade, just keep your Chase Ultimate Rewards Points in your account without spending them. To be safe, she should get the Chase Sapphire Preferred before you downgrade your Chase Sapphire Preferred, then transfer all your Chase Ultimate Rewards Points into her Chase Ultimate Rewards account. Does that all makes sense?

Hi Grant, Thanks for the update.Yes, it makes sense.

1) Can my Chase Freedom(downgraded from CSP) points be transferred to my wife’s CSP in future?

2) My wife has a credit score above 750. She is a full time mom now though. Does Chase issue CSP for house-wifes who don’t have any personal income?

I believe you can transfer Chase Ultimate Reward Points between spouses, it doesn’t matter which credit cards either of you have. I also believe in most states, you can claim household income on the credit card application form, since you are married. Lastly, Chase is supposed to bring back the Refer a Friend bonus (5,000 Chase Ultimate Rewards Points) for each person you refer that is approved for a Chase Sapphire Preferred Credit Card. You should look into that promo when it comes out in the next few weeks.

I had the Preferred for a year and I’m about to be charged the annual fee. I signed up for the Arrival+ and I’ll use that one and the Freedom for the next half a year. Should I cancel the Sapphire? I’m not sure because I read that Sapphire points are worth twice the value of the Arrival+ because when you redeem Arrival+ in non travel they are worth 0.5x.

The only reason to keep the CSP is to take advantage of Chase’s travel partners. I would say each Chase UR point is worth 1.5 cents.

Hey Grant, thanks for your quick answer. When you say travel partners you mean buying a flight in the UR portal? Can’t I do that with same airlines in the Barclaycard site? CSP’s fee is $95, so to be worth it I’d spend at least $10K in a year and get around $150 worth in UR… right?

No, Chase UR Points can be transferred to airline and hotel partners like United Airlines, Southwest Airlines, British Airways, Marriott, Hyatt, Ritz-Carlton, IHG, etc. In most cases, you get more value out of your Chase UR Points by transferring the points to those programs and using those programs to book award flights or reward nights. Check out this post for more info: http://travelwithgrant.com/how-to-guides-airlines-miles-points/chase-ultimate-reward-points/

I can’t say if the CSP’s $95 annual fee is worth it, but you will have to decide for yourself.

Hi Grant, I know this is an old post, but I’m facing this decision on my husband’s CSP. He is a reluctant participant in this, and has loved the customer service on the CSP. I would like to downgrade his CSP to a Freedom card, and then reapply for the CSP (for the bonus) in about 6 months. We would have safely passed the 24 months since the last bonus was received for the CSP product. Is there any way that downgrading this account to the Freedom could jeopardize an approval for a new CSP? Thanks!

You should be fine to downgrade the Chase Sapphire Preferred to the Chase Freedom. Some reps won’t let you make that downgrade though. If that happens, you can downgrade from the Chase Sapphire Preferred to the Chase Sapphire (basic) and then downgrade again to the Chase Freedom. Your husband should have no problem getting approved for the Chase Sapphire Preferred again in a few months and receive the new sign up bonus. Good luck!