Good morning everyone, I hope you all had a great weekend. A few days ago, Chase announced the Chase Freedom Q4 merchants (Walmart and department stores) and you can now activate those bonus categories for your Chase Freedom Credit Card. Unfortunately, those bonus categories do not excite me (there are no Walmart stores close to San Francisco), so I was considering a product change from my Chase Freedom Credit Card to the Chase Sapphire Reserve Credit Card. In fact, last December, I wrote Should I Convert my Chase Freedom to a Chase Sapphire Reserve Credit Card? I have applied for the Chase Sapphire Reserve Credit Card in the past, but I was declined based on the 5/24 rule, but I still really wanted the credit card, despite not being able to get the sign up bonus. In this post, I will explain my reasoning for the product change and show how quickly the product change is processed by Chase.

The Chase Sapphire Reserve Credit Card has a $450 annual fee, but comes with a $300 annual travel credit, 3x Chase Ultimate Reward Points on travel and dining (my 2 favorite categories), along with the ability to redeem Chase Ultimate Reward Points for travel at 1.5 cents per point. I already have a Chase Ink Plus and Chase Ink Cash, so I am familiar with the Chase transfer partners, but I am really looking forward to buying airfare and paying with Chase Ultimate Reward Points.

For the last few years, I have been using my Citi Premier Credit Card as my go to travel rewards credit card because I earn 3x Citi Thank You Points on travel. Unfortunately, due to the changes to the Citi Prestige Credit Card (mainly losing the ability to redeem Citi Thank You Points for 1.6 cents per point for American Airlines flights), I product changed my Citi Prestige Credit Card to the Citi Dividend Credit Card a few months ago. Therefore, my Citi Thank You Points are only worth 1.25 cents per point toward travel. I have less than 20,000 Citi Thank You Points, so I will save those points until I need to transfer the points to a Citi Thank You Points travel partner. I will downgrade my Citi Premier Credit Card to the no annual fee Citi Preferred Credit Card and save $95 on the annual fee.

Lastly, another dagger to my travel portfolio is the upcoming devaluation of US Bank FlexPoints. Currently, you can get ~2 cents per point on paid airline tickets, but that is changing to 1.5 cents per point beginning January 1, 2018. I am also in the process of redeeming all my US Bank FlexPoints by December 31, 2017, so the ability to transfer US Bank FlexPoints between accounts will be very useful. I have ~18,000 FlexPoints, so I need to earn 2,000 more FlexPoints in order to book an airline ticket up to $400. I will downgrade my US Bank FlexPerks Gold American Express Credit Card to the no annual fee US Bank FlexPerks Select+ American Express Credit Card and save $85 on the annual fee.

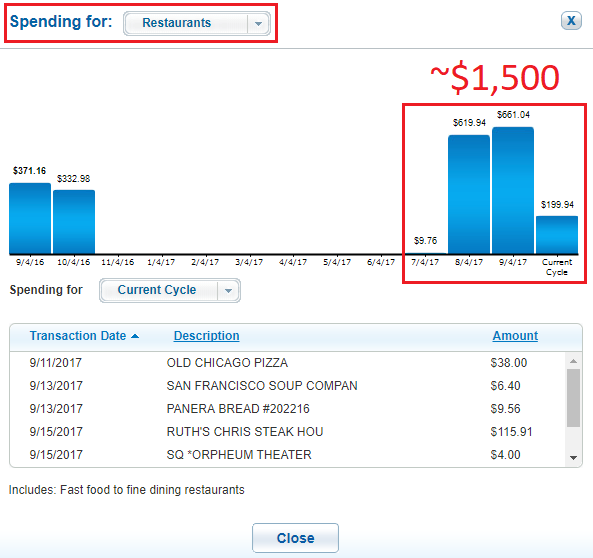

With all that said, I wanted to make sure I spent $1,500 on my Chase Freedom Credit Card in the Q3 bonus category of restaurants before I product changed to the Chase Sapphire Reserve. A few weeks ago, I wrote how to check your Q3 restaurant spending: Chase Freedom Q3 Restaurant Spending (Blueprint vs. Ultimate Rewards Dashboard). I did the same thing yesterday by clicking on the Go To Blueprint link under my Chase Freedom Credit Card.

Based on the Chase Blueprint tool, I spent ~$1,500 at restaurants in Q3 on my Chase Freedom Credit Card. There are a few restaurant purchases still pending that should post soon.

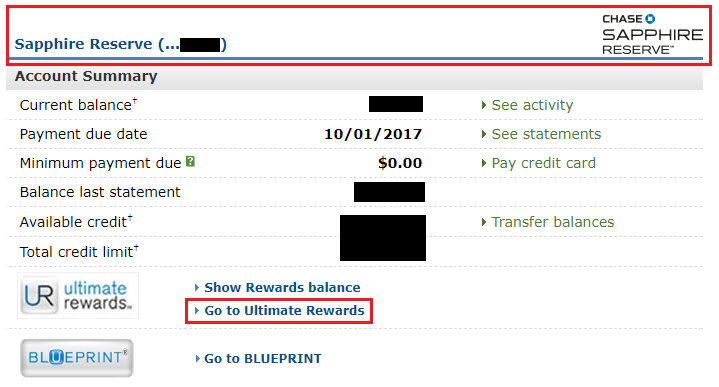

I decided to pull the trigger and called Chase. I spoke to the rep and explained that I wanted to product change my Chase Freedom Credit Card to a Chase Sapphire Reserve Credit Card. I think I caught her off guard by the request, considering that the Chase Freedom Credit Card has no annual fee and the Chase Sapphire Reserve Credit Card has a $450 annual fee. She thought I wanted to product change to the Chase Sapphire Preferred Credit Card, but I told her I wanted the high end Chase Sapphire Reserve Credit Card. She then read off a lengthy script about all the changes between the two credit cards and I confirmed that I still wanted the Chase Sapphire Reserve Credit Card. After the call, I logged into my Chase online account and spotted the Chase Sapphire Reserve Credit Card where my Chase Freedom Credit Card used to be. To see if the Chase Ultimate Rewards portal showed my new credit card, I clicked the Go To Ultimate Rewards link.

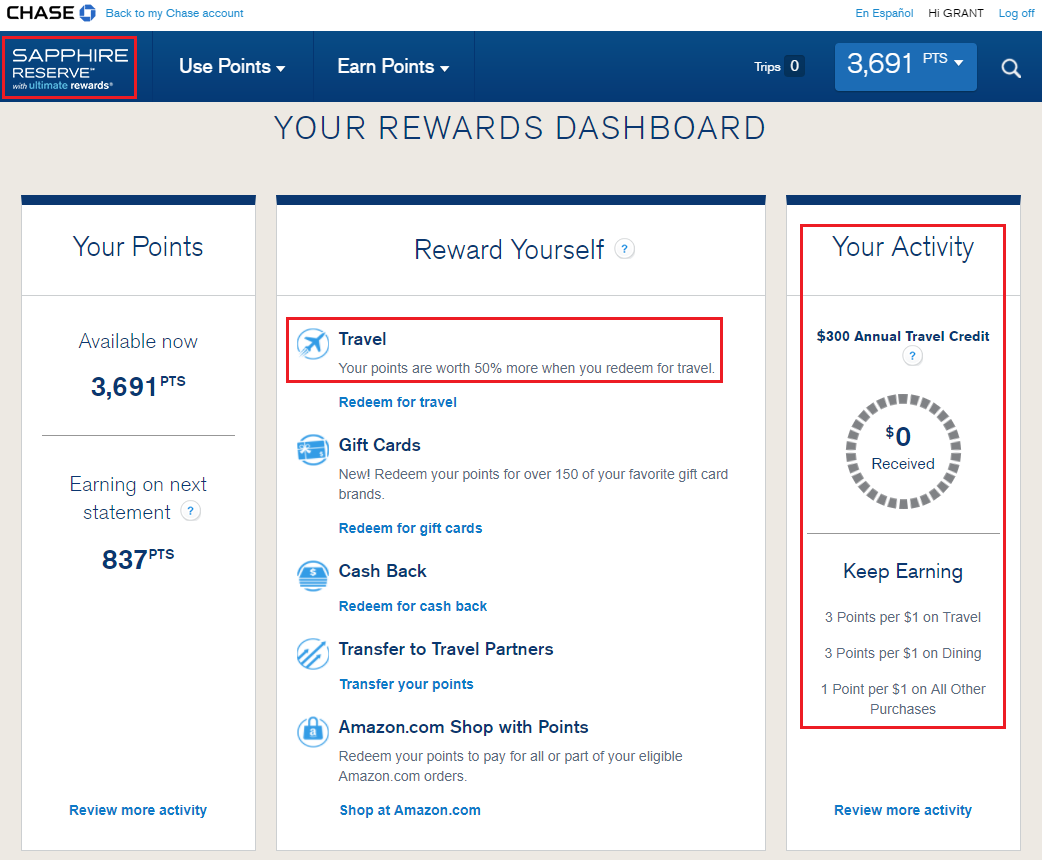

Yes, the Chase Ultimate Rewards portal showed the Chase Sapphire Reserve logo and updated account Rewards Dashboard. I look forward to spending the $300 annual travel credit and redeeming Chase Ultimate Reward Points toward travel at 1.5 cents per point. Don’t worry about my Chase Ultimate Rewards point balance, most of my Chase Ultimate Reward Points were earned by and transferred to my Chase Ink Plus, but I will need to transfer Chase Ultimate Reward Points back to my new Chase Sapphire Reserve Credit Card to book travel.

Do you think I made the right choice to product change from the Chase Freedom Credit Card to the Chase Sapphire Reserve Credit Card? Would you have done anything differently? If you have any questions, please leave a comment below. Have a great day everyone!

P.S. At one point, I had 10 Chase credit cards (personal and business), but instead of downgrading and product changing to no annual fee credit cards, I closed most of the credit cards and transferred the credit lines to existing Chase credit cards. I wish I had 2 more Chase accounts open so I could also have a Chase Freedom Credit Card and a Chase Freedom Unlimited Credit Card. Sadly, the 5/24 rule caught me off guard.

Caught a typo: “The Chase Sapphire Reserve Credit Card has a $450 annual fee, but comes with a $350 annual travel credit”

Credit is $300 (you reference it correctly as $300 later).

Let me fix, thank you for catching that typo.

“there are no Walmart stores close to San Francisco”

A little disingenuous, don’t you think Grant.

I could BART or take CalTrain to a Walmart, but it it not worth my time :)

Understand, but how many Wallyworlds do you pass by coincidentally when travelling? I just think its a flimsy justification, at best.

Anyway, we’ll agree to disagree. Have a good one! :)

I just don’t like Walmart. I have only been to a few after the Bluebird/Serve days. I’ll leave the friendly Walmart cashiers to everyone else :)

GRANT, I do believe you have indeed found a back door. Genius, sheer genius.

Thank you, it’s an unlocked back door, you just have to open it and you are in :)

This is a great idea. I think either my wife or I should go for it.

Yes, especially for a husband/wife combo, this could work out really well :)

I PCd CF to CSR last year and then PCd it back when the AF hit this year. Why? Because at that point I was the somewhat new owner of a CSP, thanks to discontinuation of the Fairmont card. Since the CSP AF wouldn’t post until next year, this seemed a no-brainer, and I’m glad I did it. Most of my CSR charges (aside from the ones using the two annual travel credits) were for food, and the CF category took care of that this quarter. Otherwise for travel, I use cards that offer higher value (i.e. co-branded hotel cards or Amex Platinum for airfare). I did like the CSR overall and will likely do a PC when the CSP AF hits. Why? I like the idea of the free roadside assistance. I recently discovered that when I use that benefit as part of my USAA policy, it posts to my CLUE report as a claim! I guess that’s within their rights as an insurance conpany. At least when the benefit is provided by a third party, that won’t happen. Anyway, congrats on your new CSR! Woohoo!

Nice to hear that you’ve been able to product change between various Chase CCs. Chase sure makes it easy to product change CCs :)

Thanks for the UR Restaurant finder tutorial!. Now only if AMEX EDP would offer the same simple supermarket segregation.

BTW CardCash eGCs via Ink/Paypal for restaurant chains is nearly always the better 5x path. Ruths Chris cost you $11.60 for the convenience of using Freedom. You’ll often find Panera for 15% off and higher. Instant delivery, and virtually no fraud risk for instant redemptions.

Yes, I agree, eGCs are usually way superior to CC rewards. I just bought a $50 Panera Bread eGC for ~15% off last week after that Panera Bread purchase. I tend to eat at a lot of chain restaurants and fast food places, so restaurant GCs are the way to go :)

Without the sign up bonus, I really see no reason to get his card. I do not understand all the hype.

The card is not for everyone, but it can make sense for others.

No more love for Citi prestige trip delay, baggage delay or lost insurance? I think it is the best in the market as of now. Despite some downgrades, Citi prestige is still the king in insurance protection. Now how useful are thankyou points is another debate.

Thankfully, I’ve never had to deal with trip delays or baggage lost/delay claims, but if that is a worry, the Citi Prestige CC is a keeper. I never used the 4th night free or free rounds of golf, so I severely underutilized that CC.

Just to confirm if I change Prestige to Dividend card can I still transfer to travel partners over time or do I have a fixed 60 days or something? Also for the $250 travel benefit can I buy airline giftcards?

Thanks in advance if you have time to answer…

To be safe, I would redeem all you Citi Thank You Points before you convert to a non-Thank You Point earning CC. I think any purchase from an airline will trigger the $250 airline credit.

I also converted my Freedom to a CSR a few months ago. Reason is simple: It’s not as easy to max out the Freedom every quarter as everyone makes it out to be. For example, this year, Q1 was gas stations. Well, I couldn’t find a single gas station (or 7-11) that would sell me a GC with a CC, so I came nowhere close to maxing out. For Q2, grocery stores was easy to max. Q3? Dining and movie theaters? I dine out quite a bit, but even then, $500 a month on dining and movies is tough to max out. And for Q4, I could buy GCs from WM, although I don’t have my Freedom anymore. So theoretically, I would have only maxed out 2 out of 4 quarters this year, which translates to 15k UR. And I can generate a lot more than 15k UR through my CSR.

I’m glad to hear your reasoning for converting from Chase Freedom to Chase Sapphire Reserve. I think Q3 was the only quarter I attempted to max out this year.

Q4 category will be easy to max without stepping foot in a walmart. Walmart.com applies and so do gift cards from there and other department stores such as Sears. No travel necessary.

I think you made a poor decision.

Oh well, I can always buy gift cards from PPDG or Staples/OD at 5x year round, so I don’t think I am missing out on much. Happy shopping :)

I got my CSR last August, and I just got hit by the annual fee of $450 last month. I was on the fence of downgrading or cancelling the card. But after some consideration, I’ve decided to keep the card. The benefits this card offers are too great to pass up. I’ve taken so much advantage of the lounge access and Global Entry, not to mention 1.5 x car rental value. I love it.

Awesome, I’m glad to hear you are getting great value out of your CSR :)

The sexy metal card is worth it in itself :)

Congrats Grant! CSR is an eye catching beautiful card to pull out … enjoy using it!

Thank you, I’m eagerly waiting for the CSR to come in the mail :)

Pingback: Redeem Chase Ultimate Rewards Points for 1.5 Cents Per Point with Chase Sapphire Reserve Credit Card

Pingback: Should I Keep Both Chase Sapphire Reserve & JPMorgan Chase Ritz Carlton Credit Cards?

Pingback: Take a Point, Leave a Point! Share your Leftover FlexPoints to Help Other Travel Hackers

Pingback: Help! Can you Convert AARP, Disney, or Amazon to Chase Freedom Credit Card?

Pingback: Keep, Cancel or Convert? Chase Sapphire Reserve & Chase Ink Plus